|

Getting your Trinity Audio player ready...

|

How will this be taxed?

As per IT Act any income from transfer of virtual digital assets will be taxed at 30%

(excluding cess and surcharge if any). Important aspects in regards to the taxability is as

follow:

- Income shall be calculated as gross receipts less cost of acquisition.

- Only cost of acquisition of such Asset has been allowed as deduction. Further, it has been specifically stated that no deduction in respect of any expenditure other than such cost, be it any allowance or set off of any loss to be allowed in computing such income from transfer of virtual digital assets.

- In addition to the above, no set off of losses arising from transfer of such assets be allowed against income from any other nature and such loss cannot be carried forward. Further losses incurred from one virtual digital asset cannot be setoff against gain from another virtual digital asset.

- Tax on transfer of virtual digital asset shall be charged irrespective of:

(a) income is below threshold limit or

(b) the assessee has sustained loss

Withholding Tax on Virtual Digital Asset in case of Resident User

A new Section 194S has been inserted in the IT Act to provide for TDS on payments for

transfer of virtual digital asset to a resident at 1% of such sum. Based on the same tax at 1%

will be deducted on transfer of crypto currency by the exchanges. Refer below flow chart for

better understanding. Such deduction will be made while making payment of consideration

to the seller.

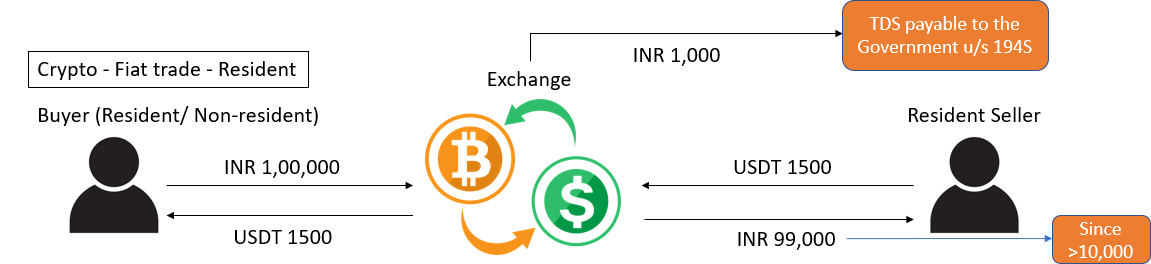

A. Example of ‘Crypto to Fiat’ Trade

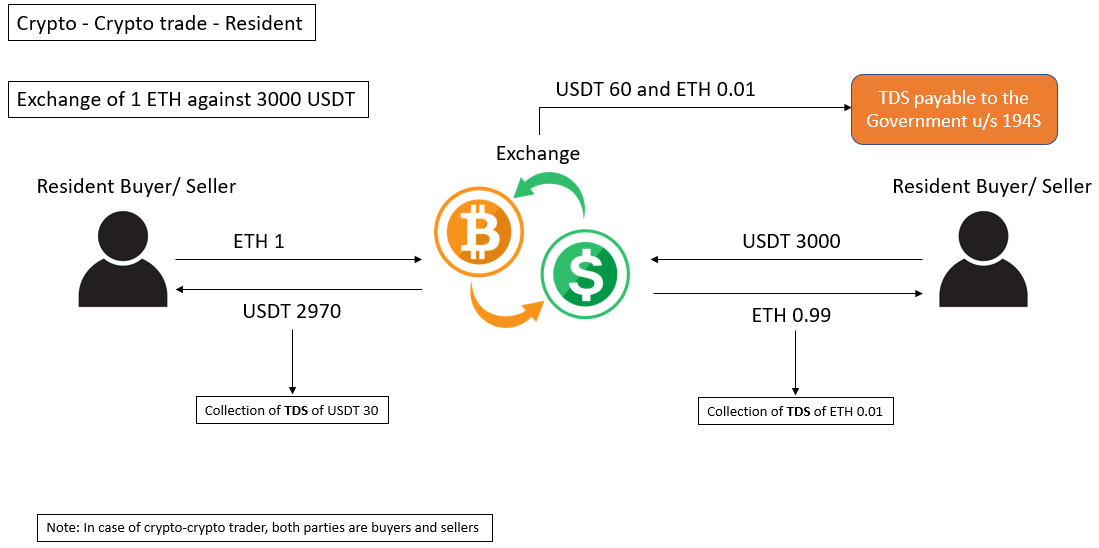

B. Example of ‘Crypto to Crypto’ Trade

Important aspects pertaining to the same are highlighted below:

- Every user will have to give declaration whether they are resident or non-resident under the Income Tax laws.

- TDS will be deducted at 20 percent rate U/S 206AA of the Act, in case of non-availability of PAN of the user.

- If the user falls within the definition of ‘specified person’, then tax at 5% will be deducted as mentioned u/s 206AB of the IT Act. ‘Specified person’ for the above means a person who has not furnished the return of income for the assessment year relevant to the previous year immediately preceding the financial year in which tax is required to be deducted and the aggregate of tax deducted at source and tax collected at source in his case is rupees fifty thousand or more in the said previous year

- If users are exchanging VDA against another VDA, then TDS will be deducted in the form of VDA and net quantity will be delivered in your account.